When is Tax Loss Harvesting worth it? + How to, Mistakes, and Benefits

What is tax-loss harvesting?

Selling positions in a loss. Then, immediately replacing a position with a similar, but not *identical security. A loss offsetting future portfolio income or gains, or real estate and business capital gains.

Also, you can use up to $3,000 of the losses (*married filing jointly – “MFJ.”) to offset earned income, as well. However, married filing separately filers are penalized and limited to the $1,500.

**Please note, tax-losses do NOT ALL not to be used in the year they are harvested, and can be used. You can roll them forward until death.

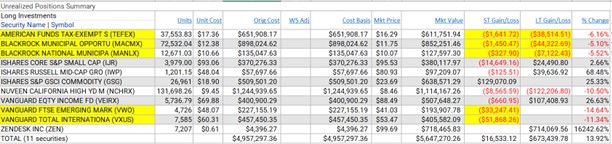

Let’s take an example:

(Eric note: I did not have complete control of constructing this portfolio. Legacy positions transferred in.)

Highlighted are positions tax loss harvested. These positions were sold, and we replaced them with like securities that weren’t “substantially identical.”

- For example, In the above portfolio I sold American Funds Tax-Exempt S – TEFEX. Replacing it with Vanguard California Long-Term Tax-Exempt VCITX.

—-//>>

Example Benefits

In this account example we tax loss harvested ~$179,000. Total, we have harvested $1.1MM in this client’s taxable accounts this year.

At this client’s long-term capital gains tax rate, including their state tax bracket in California, the tax savings is close to 30% to 40% on the dollar. That’s an estimated $330,000 to $440,000 in tax savings. *This estimate assumes losses are meet or exceed the yearly gains in their portfolio, business, or real estate, or they stay in that bracket.

There is also a large long-term capital gain in ZEN of $714,000. If the ZEN stock is sold, to reduce concentration risk, and a gain is generated, it will then push this client into the top capital gains rate, and in top state tax rate for California, or about 30%. So roughly $214,000 in taxes will be incurred to sell that position.

But, based on the tax loss harvesting this year, if that position is sold this year, no taxes will be paid on the gain.

Estimated savings – around $214,000 in taxes.

Where are most investors confused about tax loss harvesting?

- Taxable accounts only, no retirement accounts, this is only allowed in your non-qualified accounts.

- For example, your joint account is down $20k, your IRA is down $50k, and your revocable trust is down $17k, you can tax loss harvest $37k. Losses in your IRAs, 401(k)s, or any retirement accounts can’t be harvested.

- Indefinitely roll forward the losses, if investors don’t have significant gains to offset this year, they can use up losses when we they are in a higher tax bracket. Indefinitely rolling the losses to future higher income years.

- For example, you sell iShares Core S&P 500 ETF – IVV for a $19,000 long-term capital loss this year, but you have no capital gains to offset. So, you wait another 3-years until you sell your rental property and have a long-term gain of $20,000, using the $19,000 to bring the gain down to $1,000.

- Tax brackets matter, there’s a larger benefit for a CA investor in the highest tax bracket, than someone in TX that is under the capital gains threshold for paying taxes (currently, this capital gains tax threshold is around $80,000 for married filing jointly).

- For example, if you live in a state with no income tax like Texas, and make under the $80k in income, your capital gains rate is zero. Therefore, while there’s a small benefit to offsetting short-term capital gains counted as income for federal taxes, it’s a lot less than a California investor in the top tax bracket.

- $3,000 against your earned income (i.e., W2, 1099, Etc.), you can use the losses to offset your capital gains: investment portfolio, business, and real estate capital gains. But, only offset $3,000 (MFJ) in earned income per year.

- For example, in the above case, I harvested $179,000 in losses. If the client had no capital gains to offset, I could only reduce their earned income by $3,000, and roll the remaining ($179,000 – $3,000 = $176,000) $176,000 forward, against future losses.

What are some mistakes investors make when tax loss harvesting?

- Not tax-loss harvesting at all, A lot of high-income tax bracket investors are busy making money. To many of their credit, when the market is down, they buy more. But they don’t sell their losses to offset taxes. And over time, this can create huge long-term capital gains in positions.

- For example, an investor owns $100,000 in SPDR S&P 500 SPY – ETF. It’s fallen 20%, and has a $20,000 loss we can take. We could replace it with Vanguard S&P 500 ETF – VOO, a close substitute. Instead, the investor buys into more SPY with cash at a lower price.

- We could have used that $20,000 loss in the future against any gains. If they are in the 40%ish tax bracket all in Colorado with state income for short-term gains, we are forgoing $8,000 in tax benefits.

- You can imagine how much this adds up with a large amount of taxable accounts if the market is down on average 14% intra-year every year, and you don’t tax loss harvest.

- We could have used that $20,000 loss in the future against any gains. If they are in the 40%ish tax bracket all in Colorado with state income for short-term gains, we are forgoing $8,000 in tax benefits.

- For example, an investor owns $100,000 in SPDR S&P 500 SPY – ETF. It’s fallen 20%, and has a $20,000 loss we can take. We could replace it with Vanguard S&P 500 ETF – VOO, a close substitute. Instead, the investor buys into more SPY with cash at a lower price.

- Wash sale rule, you can’t buy and sell the same security in 30-days, but you can find and replace the security with something that is not “substantially identical.”(Eric Note: Because there is not a technical definition from the IRS, many investors get stuck here, and lack the confidence to pull the trigger.)

- For example, you can’t sell Apple stock, and then go back right away and buy Apple stock next week. Or, sell the Vangaurd Total Market ETF – VTI, and buy the exact same Mutual Fund Vanguard Total Market – VTSAX right away. Both violate the wash-sale rule. A more nitty gritty, you technically are not also allowed to buy back the position in an IRA, though this might be harder to track (just saying).

- Staying in cash for 30-days to avoid a wash-sale rule, I’ve heard of horror stories from other advisors in my peer group, and the TD Ameritrade trade desk that “experienced advisors” do this. Committing a cardinal sin of selling low and buying high.

- For example, you sell $250k of Invesco QQQ Trust Series – QQQ at a 30% loss, and don’t rebuy into the market until 30-days pass. So, while you have $75,000 in losses to offset. Over 30-days, QQQ increases 20%, and you miss out on $50,000 in gains.

- Non-suitable alternatives, sometimes you might want to tax-loss harvest a security, but the strategy or position has a large decline, plus there’s not another manager, strategy, position that is close enough to the risk/return allocation. So, in doing this you’d be selling low and buying high.

- For example, the Nuveen California High Yield Municipal Bond Fund above in the example is down 17%. In my professional opinion, there are not similar strategies with close enough risk/return tradeoffs. So, if I sell, I’ll get the tax loss. But might sacrifice real gains as the position climbs back fast than a similar less risky alternative, down less.

- Infrequent or too frequent, Many potential clients tell me they don’t tax loss harvest. Worse, some advisors confess to me they don’t do it either! Even though it’s advertised! Yikes. Others obsess daily over a few dollars to sell. Remember, If you tax-loss harvest right away without letting losses build up, you’ll run out of alternatives. That’s a no-no. Having a system of how frequently you look for loss, knowing alternatives in advance, having a minimum dollar amount, and convicting break the rules you just set, are important!

- For example, Let’s say Vangaurd Intermediate Bond ETF – BIV is down $2k, and you sell it and replace it with iShares Intermediate Govt/Credit Bond ETF – GVI, and now GVI falls. GVI is in a $1k loss in under 30-days. So, you sell again. Wait? What do you buy back into now? If you keep doing this, you’re going to run out of close alternatives to replace your intermediate bond position, and/or create a mismatch in your portfolio.

- Oversimplified portfolio allocation: Target date funds, can limit the ability to tax loss harvest if one of the asset classes is down and another is up. This is not as much an issue when everything goes up and down together, but as interest rates rise asset class correlations, have fallen over time. Bonds might be up. Stocks might be down, and vice versa. So, if it’s all combined in one portfolio pot pie there might be no benefit.

- For example, let’s say bonds are down 10%. Stocks are up 10%. You own a Target Date Fund with a 50%/50% split between bonds and stocks, so there’s no loss. Let’s say you own a bond ETF, and stock ETF at $50,000 each. You can tax-loss harvest the $5,000 ($50,000 * -10% = $5,000) loss on the bond fund versus not having any benefit in the target date fund.

- Target-date funds can also accumulate huge gains over the long-term, making it also harder to tax-loss harvest.

- For example, let’s say bonds are down 10%. Stocks are up 10%. You own a Target Date Fund with a 50%/50% split between bonds and stocks, so there’s no loss. Let’s say you own a bond ETF, and stock ETF at $50,000 each. You can tax-loss harvest the $5,000 ($50,000 * -10% = $5,000) loss on the bond fund versus not having any benefit in the target date fund.

- Overcomplicated portfolio allocations: Direct indexing, or Oversold benefits for an Asset management fee, many Robo(t) Advisors use this as the main value for paying an asset based fee.

Recently, many major brokerage shops (i.e., Fidelity, Vanguard, Charles Schwab) have or will release “direct indexing.” Here’s the breakdown: instead of owning an ETF that tracks a benchmark you own *most the underlying stocks in the benchmark. Software then monitors each position daily, weekly, or monthly for tax loss harvesting each position. In period of market stress, if certain securities or sectors fell a lot in value, the benefits could add up a lot more than if you just owned the ETF.

However, over time they direct index portfolios get complicated! Many clients end up owning hundreds of stocks with gains. At that point, you might have a hard time selling all these new gains. Then, with all the positions it’s harder to manage. Plus the asset based fee you are paying.

-

- For example, instead of owning iShares Core S&P 500 ETF – IVV, you own the direct indexing S&P 500 through Fidelity. Their software puts you in 250 stocks. The first year they harvest $20k in losses on your $250k account. But after the third year, there are so many long-term capital gains, you can’t harvest anything, and now you are stuck in a portfolio with 250 positions that is complex and hard to manage, plus you are paying 1%.

Bottom-line

Tax loss harvesting adds future portfolio flexibility and a war chest against capital gains in a business, real estate, or your portfolio. In addition to interest, income or short-term capital gains in your portfolio that creates taxable income every year.

Equal important, It also helps investors sell concentrated or low basis stock to reduce risk without having to worry about a large tax bill.

The wonders of tax-loss harvesting.

*One finer point (Damn Eric really!?) Mismatches with settlement/pricing and trading can also occur if you are buying and selling mutual funds and ETFs (Exchange Traded Funds), and not going from an ETF to ETF, or mutual fund to mutual fund.

Mutual Funds to Mutual Funds, Mutual funds can be transferred or exchanged into other mutual funds. No biggie. This is the cleanest process. But, most investors hold ETFs for their cost advantage though.

ETFs to ETFs, also, ETFs trade intra-day. If it’s a volatile day, and you sell an ETF, then, immediately buy another ETF, there’s slippage with bid-ask spreads and intra-day market movements, but it might not be too bad.

Mutual Fund to ETF, the largest issue is selling a mutual fund to buy an ETF. You have no clue what the net asset value price will be at the end of the day for the mutual fund while you buy the ETF immediately. This exact same day transaction is also disallowed at certain brokerages (i.e., Vanguard). Many brokerages will not let you trade on unsettled cash. So, you trade out of the Mutual Fund and then have to wait the WHOLE next day open to buy. What if the market rallies back after-hours…And you are in cash!?

ETF to Mutual Fund, this is also an issue trading from ETFs to mutual funds. You have no clue what the exact price in the mutual fund will be at the end of trading.

Bottom-line: mutual funds to ETFs, or ETFs to mutual funds have more factors to consider.

**Disclosure: This is my interpretation of the IRS tax code as a practitioner. Calculations and outcomes are specific to each client based on their specific facts and circumstances. This is for educational purposes, and not intended to be advice. Please check with your own tax professional for your own personal situation.