Almost 50% of all US Dollars in circulation were printed in 2020

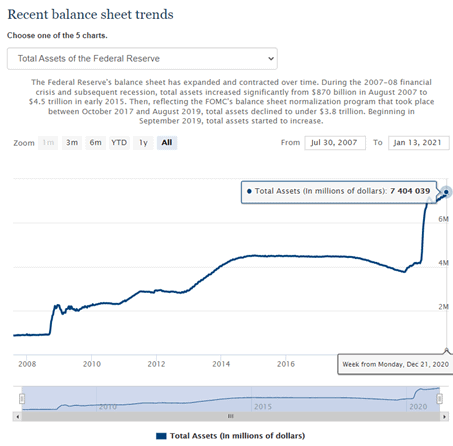

Let’s back up…In 2008, the Federal Reserve added about $2 Trillion (with a T) to the financial system. Avoid global contagion meltdowns. Avoid the next Great Depression. Avoid turning into Japan. Avoid deflation.

Fast forward 12 years. COVID-19 hits in March 2020. At this point, the Federal Reserve almost doubles the balance sheet in months. From February to September 2020, the balance sheet jumps from $4 Trillion to ~$7.5 Trillion (with a T).

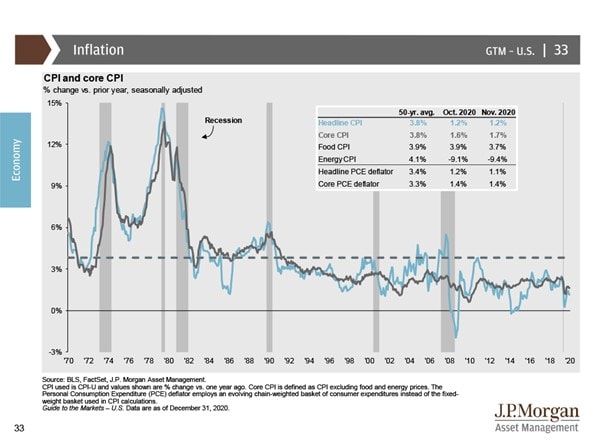

But, do we have that special inflation number the Fed is targeting? Not according to the Consumer Price Index (“CPI”), or what the Federal Reserve uses to measure inflation.

So, the CPI rests at 1.2%, as of November 2020.

But, are YOU sure that means there is no inflation? But, what for it…

Before Biden is trying to get ANOTHER $1.9 trillion dollar stimulus package passed.

Your Cost of Living ≠ Consumer Price Index

Many capital market assumptions throw around 2% to 2.5% long-term inflation assumptions like they’re etched in stone.

Sorry, as a practical matter, the Consumer Price Index as a measure of the cost of living is completely insufficient and inadequate. If we measure what people actually spend money on. And, how can we think the increase in the cost of living is the same in Wyoming as it is in Denver or San Francisco?

It’s not.

How and why did the CPI Change?

Taxes. Food. Energy. All are excluded from the Consumer Price Index, among other common items we actually spend money on. So why does the Federal Reserve, Social Security, and pensions really use CPI to measure inflation?

Did you know the original CPI calculation to measure inflation changed? Why?

It saves the government money.

In the early 1980s, the United States entered a recession. Inflation hit 13.5%. Something needed to be done. The government was going to be forced to keep increasing entitlement benefits at an unsustainable rate. Then, the calculation changed again in 1995.

Remember, Social Security currently makes up almost ¼ of the current government spending. Imagine if the government was on the hook for 10% in increased Social Security benefits per year? They couldn’t foot the bill.

“It is estimated that between 1996 and 2006, the reconfiguration of the CPI saved the US government over $680 billion.”

So, could inflation really be 10%?

Yes, according to the Chapwood Index, an alternative cost of living index that measures what people really spend money on. The Chapwood Index measures 500 of the most used items per year, by U.S. city.

Average inflation over the past 5-years:

- Denver: 7.9%

- San Francisco: 12.8%

- El Paso: 9%

- Phoenix: 8.1%

- Austin: 10.2%

So, now that you know, what can you do about it?

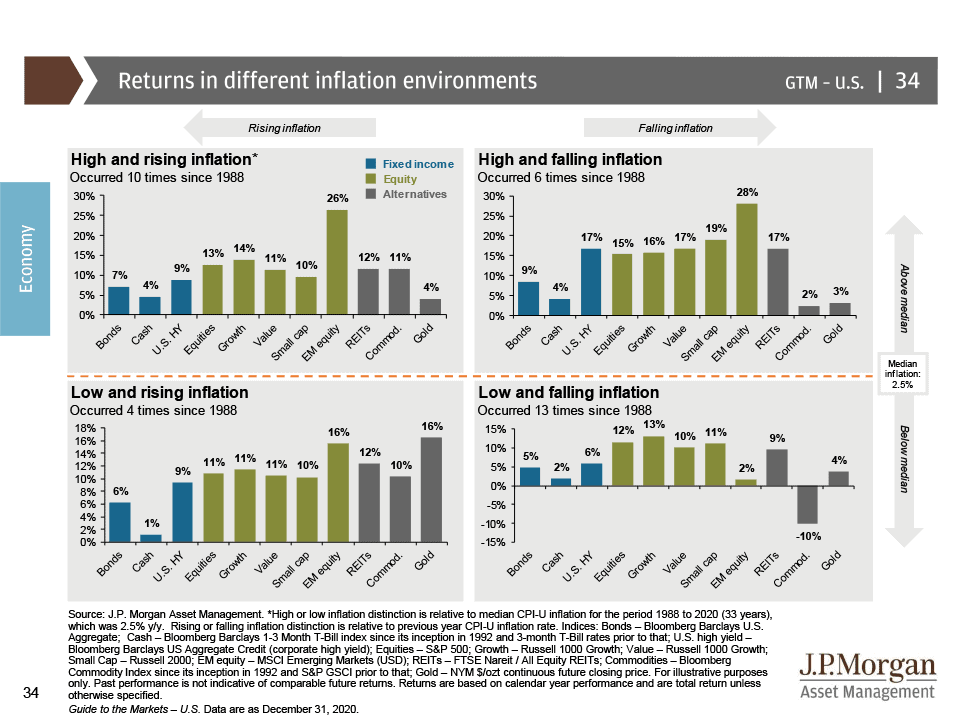

Historically, what asset classes have worked to protect us against inflation?

Treasury Inflation Protected Securities: “TIPS”

The good

I recently read an article where an advisor advocated placing 40% of an entire bond allocation into TIPS? That’s a pretty large piece of the pie, so should it be done? Their theory was TIPS increase in value as inflation, and are structured to perform well in inflationary environments (and have historically).

The bad (and ugly)

If the bond principal payment increases based on CPI, BUT we just explained that CPI does not measure the true cost of living inflation, so how does this help you? Plus, the ugly part, is that bonds have duration. Interest rate risk. So, (typically) as interest rates increase, bonds decline in value. Make sure you take into account the duration (or maturity) of the bonds if this strategy is considered.

Gold

The good

So far there’s an argument for gold. Historically, in periods of rapid inflation like in 1974, and recessions in 2008, portfolios with allocations to gold performed better.

The bad (and ugly)

However, what if gold is not reacting to inflation the same way it did in the past? Yes, in 2020, gold returned 25%, but what will it do in the future? And year-to-date 2021, it has underperformed other commodities. Also, could investors view digital currencies like Bitcoin as a better alternative, and rotate into this instead of gold?

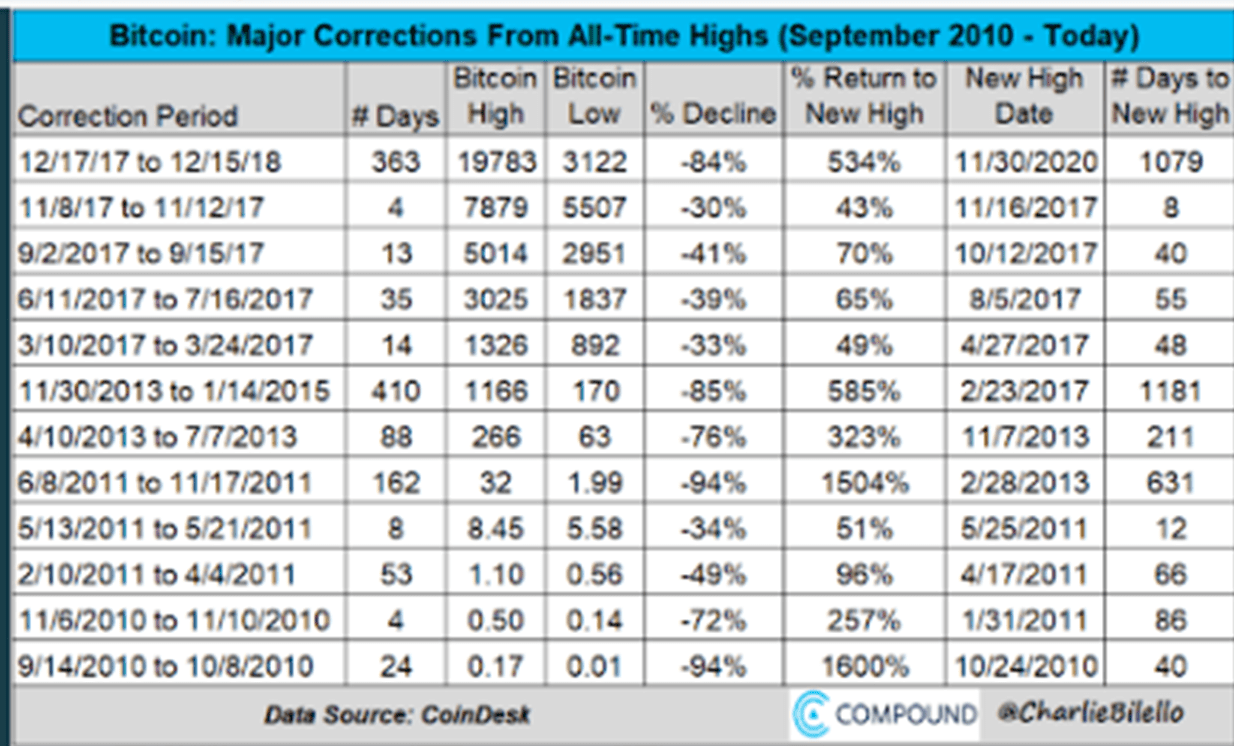

Bitcoin and digital currencies

The bad (and ugly)

Ask advisors over age-50 why they don’t invest in digital currencies: fraud, poor storage of value with crashes, it’s not a “real” asset, and the only asset “lost” with a forgotten password….Ahem….Plus they can’t get paid to advise on it because of the way an Assets Under Management pays the advisor. Plus, there’s a giant career risk, and lack of education. Most will pass.

The good

Better yet, ask them what are the benefits of digital currencies? Do they own any? If it is a fraud, why do some of the most successful entrepreneurs (Jack Dorsey) and old companies like Mass Mutual allocate to it Bitcoin? Again, could this bias be that advisors can’t get paid an asset under management fee, or because they really don’t see any merit?

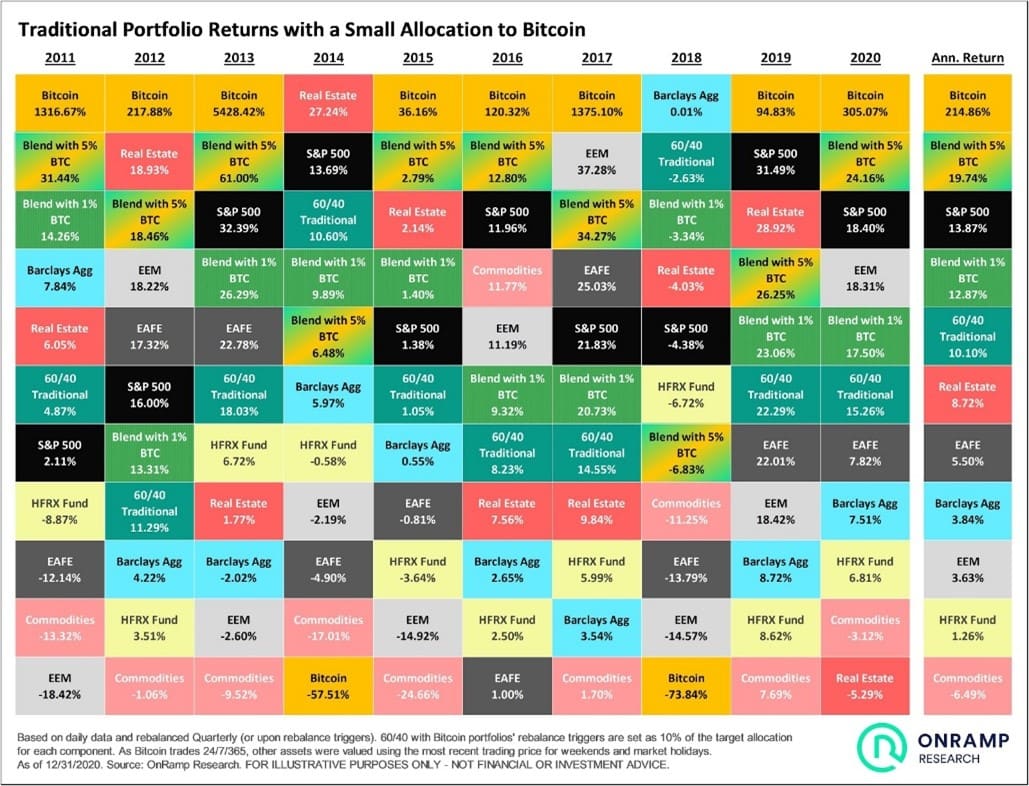

What if you just had a 5% allocation since 2011?

Historically, that would of worked very for you.

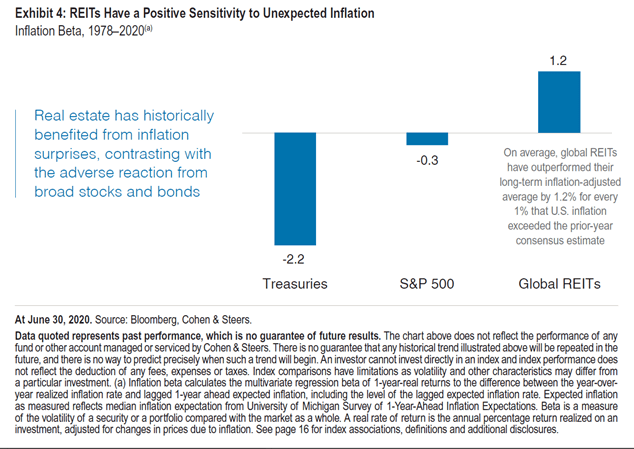

Real estate

The good

What about more Real Estate Investment Trusts (“REITs”) or directly held real estate? Yes, there are moratoriums with rent collection (in some areas of the country), and malls may never recover. But as the saying goes, “they are not making any more land.” Right?

The bad (and ugly)

REITs suffer as interest rates increase, so what about with interest rates at historical lows? How will that affect a lot of illiquid assets?

The ugly, private real estate deals are en vouge. Again. Investors want something different than the “stock market.” So, may believe these types of investments lack volatility. They don’t.

They lack liquidity.

So, price declines don’t flash on a screen everyday, or show up on a statement, like REITs.

With so many high fees, some of these private real estate deals create great investments for the sponsors/general partners. Yet, the limited partner (you) might be in a position where you get market returns with less liquidity just to be a part of the “not in the stock market” club.

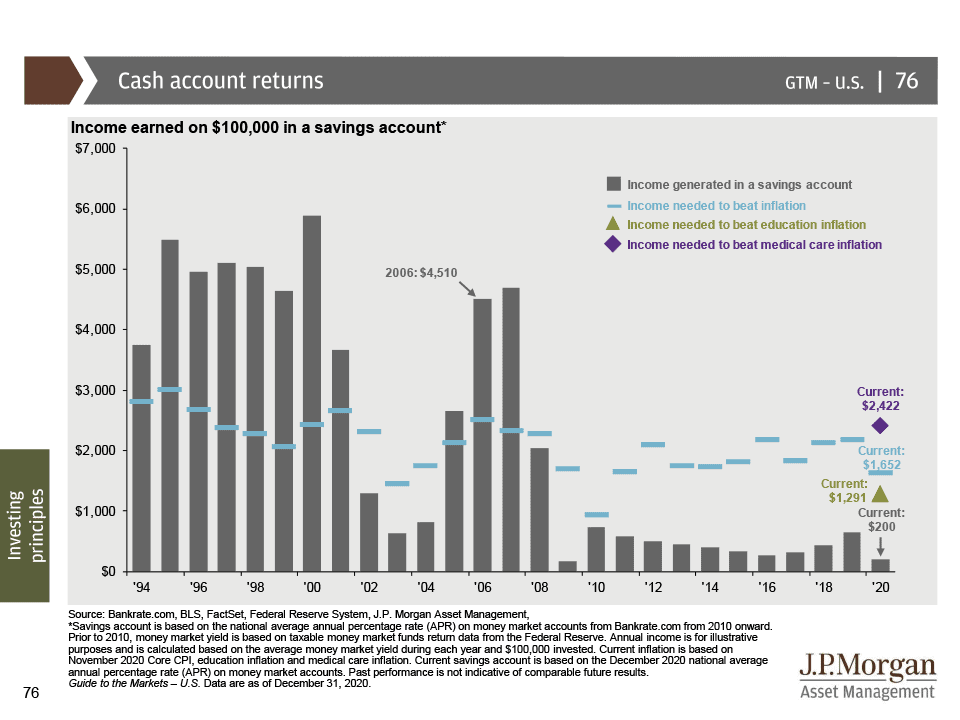

Cash

The good

Some advisors think it’s best to have more cash, because they want to deploy it during higher volatility, or where there are better price opportunities to buy into “cheaper” assets versus bonds.

The bad (and ugly)

But, there’s an issue with that, the dollar is declining in value, and waiting around for the next best buying opportunity could be costing you a lot of money in opportunity cost…inflation.

And, there’s more

Portfolio tweaks we haven’t discussed: Lowering duration on all your bonds. Adding or increasing high yield bonds, commodities, emerging markets stocks. BUT, all are not without risk. And, just because things have worked historically, does not mean they will continue in the future.

What can you control, and what does this mean for you?

Does this mean that you need to allocate more to gold or real estate? Keep less cash for your emergency fund? Invest more aggressively? Buy cryptocurrency?

Maybe, maybe not.

We don’t know your situation.

But at some point we are going to have to realize that it’s blatantly clear we have to do something different, and that might be different for everyone.

Start by asking yourself…

- Do you truly understand your cost of living?

- Do you track your personal expenses and can you see this?

- What are the assumptions your financial advisor is using to calculate inflation? Are they just accepting the same assumptions made 30-years ago?

- Have you stress tested what would happen to your plan if inflation was just 2% higher than estimates?

- Have you looked into alternative asset classes, and at least understand the trade-offs?

- Do you understand how your advisor gets paid?

- Because if they are paid based on asset-based fees, the incentive is to keep you in an account only they can make money on versus something else that might protect you better against inflation.

Crystal balls versus a blast from the past

Just because there isn’t a simple answer, does not mean that you don’t have choices. Or, that you can’t take action to learn more, and protect yourself.

The worst thing you can do is accept everything that worked in the past will work in the future, or that everything in the future won’t reflect the past.

It won’t.