A 457(f) plan is taxed at vesting, not at payout. The full value of the benefit becomes ordinary income in the year your risk of forfeiture lapses, even if you do not receive a dollar of cash until years later. This single timing rule is the most important and most misunderstood feature of these plans, and getting it wrong can turn a generous benefit into a tax bill that arrives years before the money does.

If you are a senior leader at a university, hospital, or other tax-exempt employer, a 457(f) is often the centerpiece of your supplemental compensation. It behaves very differently from the deferred comp your peers in the corporate world deal with. Understanding when the tax is paid is crucial for planning that builds your wealth versus one that quietly works against you.

What a 457(f) plan actually is

A 457(f) is a nonqualified deferred compensation arrangement offered by tax-exempt and governmental employers for a select group of senior people: controllers, treasury VPs, deans, endowment leaders, and similar senior roles at universities. It is often called a “top-hat” or a Supplemental Executive Retirement Plan “SERP” arrangement. It allows an employer to contribute above the normal retirement plan limits for retention purposes.

The “f” distinguishes it from the more familiar 457(b). Where a 457(b) has contribution limits and more favorable, payout-based taxation, a 457(f) has no contribution ceiling, which is exactly why employers use it to deliver large, targeted benefits. That flexibility comes with a tradeoff written into the tax code, and it behaves nothing like its better-known cousins. That is where planning misunderstandings and mistakes are made.

The rule that surprises people: taxed at vesting, paid at payout

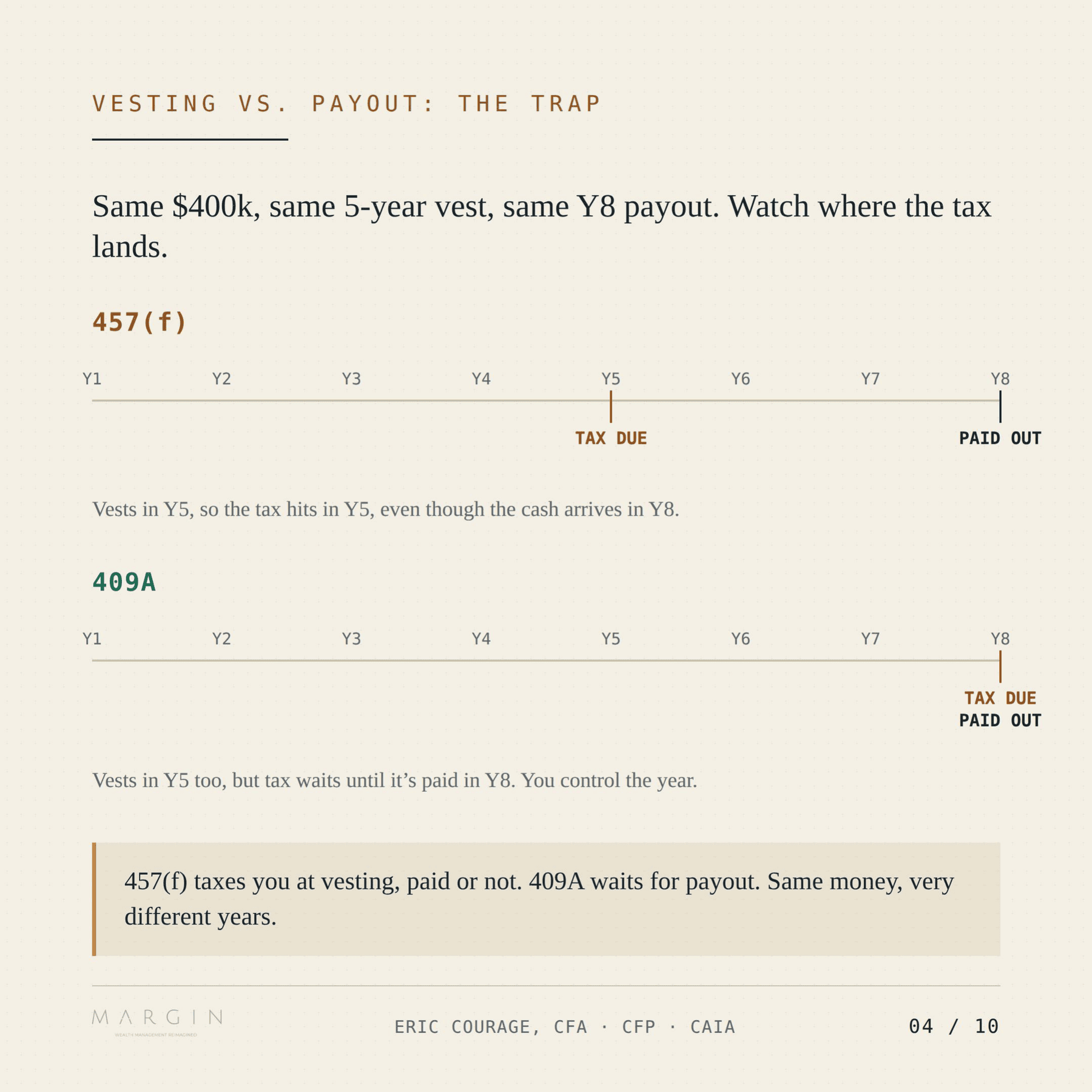

To defer the income, the plan must carry a “substantial risk of forfeiture.” In plain terms, you have to be at genuine risk of losing the benefit, usually by being required to stay employed through a certain date or hit a performance-defined milestone. The moment that risk is gone, the IRS treats the money as earned, whether or not you have been paid.

That creates two distinct moments that often fall in different years:

The vesting date is when your risk of forfeiture lapses. This is when the entire vested amount is included in your ordinary income.

The payout date is when the cash actually reaches you. This can be the same year or several years later, depending on how the plan is written.

The tax follows the vesting date. So you can owe ordinary income tax on a six-figure benefit in a year when your actual cash from the plan is zero. Compare that to a 409A corporate plan, which generally taxes you when the money is paid out, giving you far more control over the year.

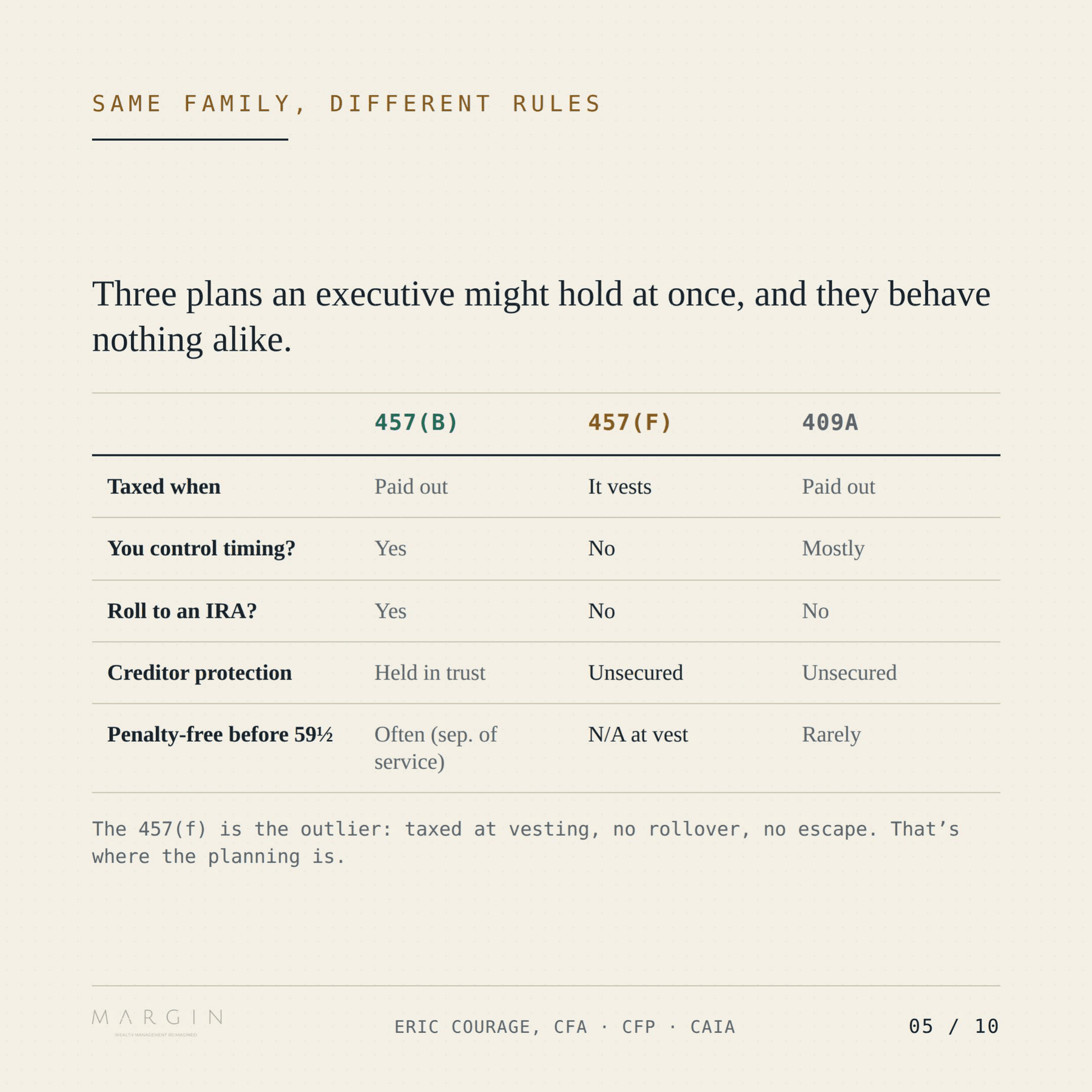

Same family, very different rules

Many executives hold more than one of these plans at once and assume they all work alike. They do not.

Here is how the three most common arrangements compare:

| 457(b) | 457(f) | 409A | |

|---|---|---|---|

| Taxed when | Paid out | It vests | Paid out |

| You control timing? | Yes | No | Mostly |

| Roll to an IRA? | Yes | No | No |

| Creditor protection | Held in trust | Unsecured | Unsecured |

| Penalty-free before 59½ | Often (separation of service) | N/A at vest | Rarely |

The 457(f) is the outlier: taxed at vesting, no rollover, no escape. That is precisely where the planning work lives.

One point in the 457(f)’s favor that often gets overlooked: distributions are not subject to the 10% early-withdrawal penalty that hits many qualified plans before age 59½. The catch is that everything is taxed as ordinary income at vesting regardless, so the absence of a penalty is helpful but does not change the core timing problem.

Worth noting too: payroll taxes follow the same vesting trigger. FICA and Medicare apply to the full benefit value at vesting, not at payout. The Social Security portion is usually already maxed out by the time a senior executive’s plan vests, but the Medicare surtax can still add to the spike, and it is one more thing to plan withholding around.

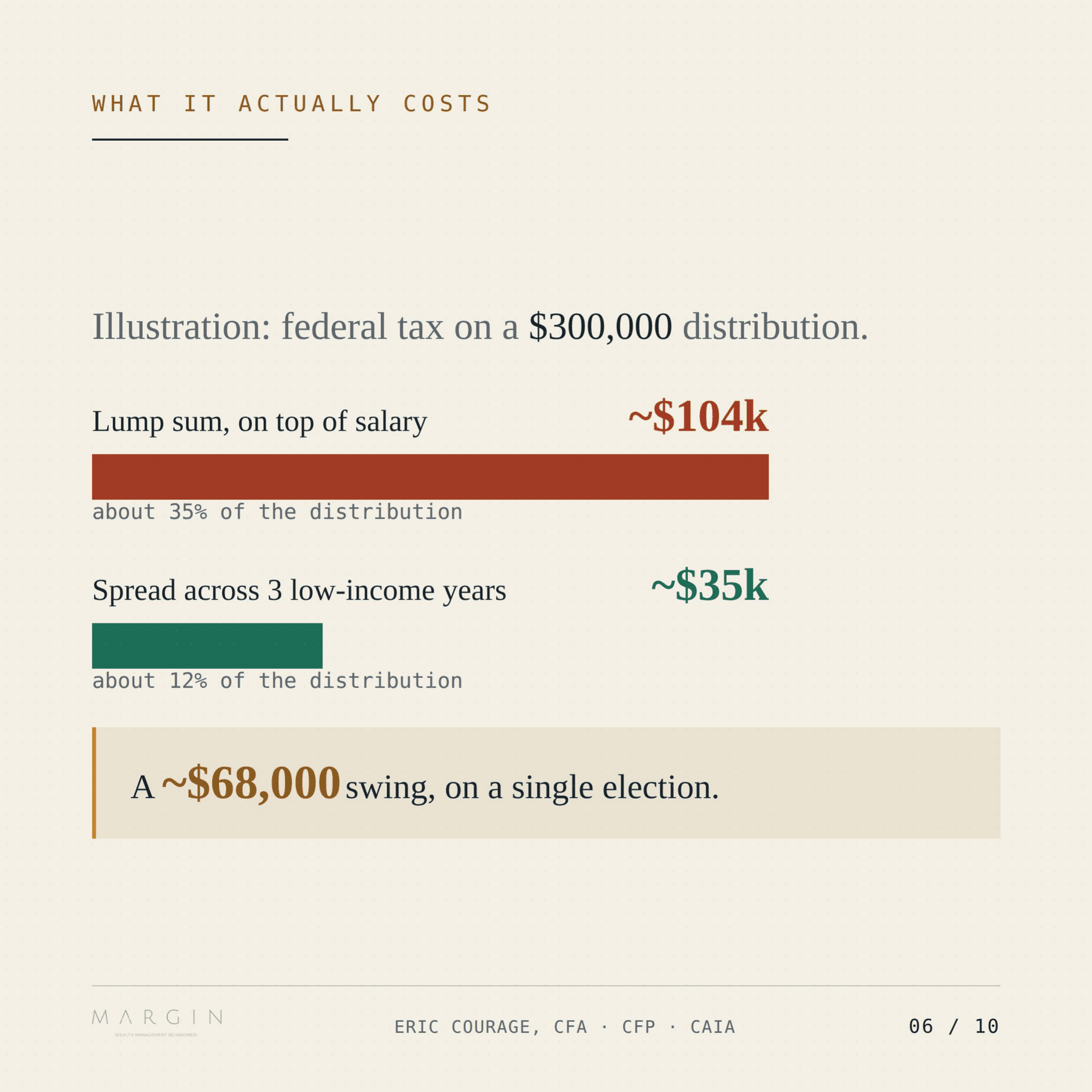

What it actually costs

The dollars make the point better than the rules do. Take an illustration of the federal tax on a $300,000 distribution.

Taken as a lump sum on top of peak salary, the tax runs roughly $104,000, about 35% of the distribution, because it stacks on top of already-high income and lands in the top brackets.

The same $300,000 spread across three lower-income years comes to about $35,000, or about 12%, because each slice is taxed at lower rates.

That is roughly a $68,000 swing on a single decision about timing. With a 457(f), the at-vesting rule means that the decision is made in the plan’s vesting schedule, not at payout, which is exactly why the terms you negotiate up front and the years leading into vesting matter so much.

These figures are illustrative and for general education only. Actual results depend on your income, filing status, and state of residence.

Where a 457(f) bites

Several structural features make this plan riskier than it looks:

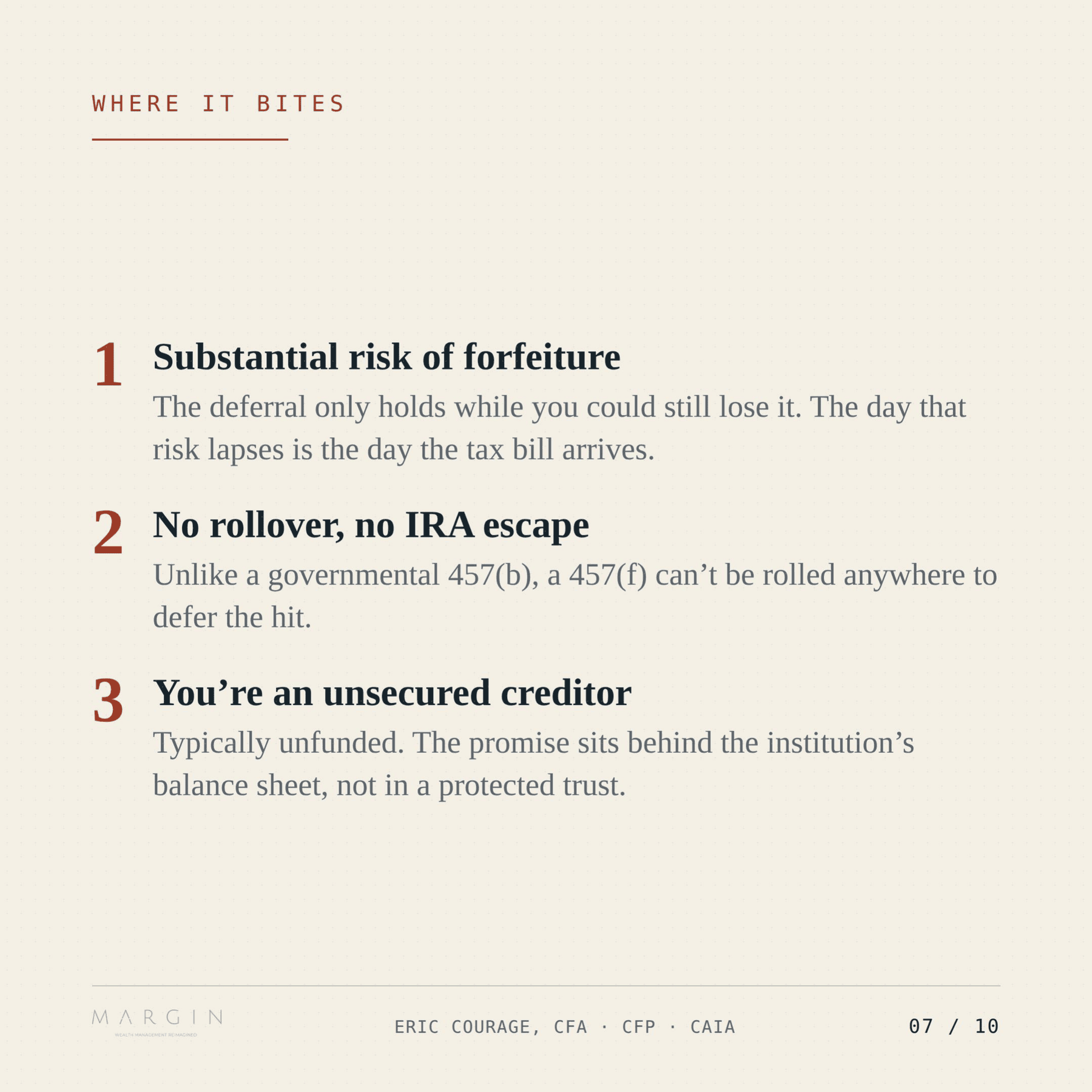

- Substantial risk of forfeiture. Deferral only holds while you could still lose the benefit. The day that risk lapses is the day the tax bill arrives.

- No rollover, no IRA escape. Unlike a governmental 457(b), a 457(f) cannot be rolled anywhere to defer the hit.

- You are an unsecured creditor. These plans are typically unfunded. The promise sits behind the institution’s balance sheet, not in a protected trust, so the financial health of your employer matters. Plans can use a “rabbi trust” to set the money aside, which protects you if the employer simply changes its mind or is acquired, but not if the employer goes insolvent. In bankruptcy, you stand in line with the other creditors. A rabbi trust is comfort, not protection.

- A layoff or merger can detonate the tax bill early. Read the acceleration clauses before you ever need them. Many 457(f) plans vest in full on an involuntary termination without cause, a resignation for good reason, death, disability, or a change in control of the institution. That means a layoff or a merger can trigger the entire tax on the full benefit in the same year you receive a severance package, stacking one large income event on top of another at the worst possible moment. The time to understand your acceleration triggers is while you are still comfortably employed, not in the middle of a separation.

- A weak forfeiture condition can collapse the whole deferral. The IRS defines a substantial risk of forfeiture narrowly. If the arrangement does not meet that standard, the deferral can be taxed immediately when the compensation is promised, rather than years later at vesting. That eliminates the entire tax-deferral benefit and can put the arrangement on the radar for an audit. As a rule of thumb, advisors generally look for at least 2 years of required future service for the deferral to hold up, and the work required must be substantial relative to the size of the benefit. This is why how the plan is drafted matters as much as the headline number.

One more piece of context: your employer’s excise tax

This one is not your tax bill, but it shapes what your employer can offer. Tax-exempt organizations face a 21% excise tax under Section 4960 on compensation above $1 million paid to certain employees, and 2025 legislation broadened who that applies to. Because the tax is measured in the year compensation vests, a large 457(f) balloon vesting in a single year can create a sizable bill, paid by the institution, not by you. The practical effect is that boards and compensation committees are increasingly cautious about how these plans are structured. Knowing this helps you read the constraints your employer is working within when a plan is designed or renegotiated.

The planning that offsets it

- Because the vesting date is usually known well in advance, the work happens in the years leading up to it, not after. The catch with a 457(f) is that the spike is ordinary income, and very little offsets ordinary income dollar for dollar. That makes the order of these levers matter. Here they are, strongest first.

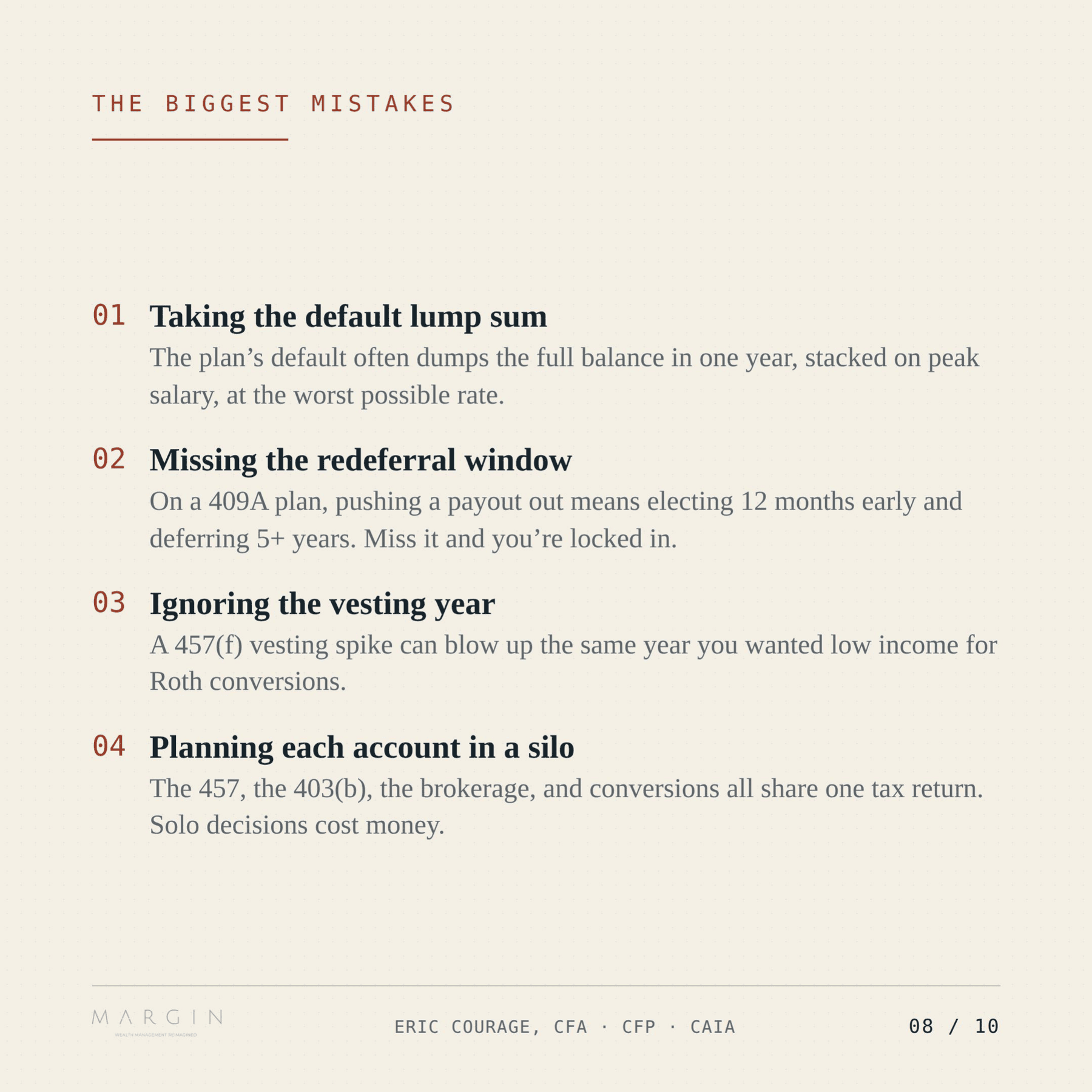

Negotiate the vesting schedule before you sign. This is the one most people get wrong, and it is the highest-leverage move by a wide margin. With a 457(f), spreading the cash payout after vesting does not reduce the tax, because the whole benefit is taxed the moment it vests. In fact, many plans are built as “short-term deferral” arrangements that must pay out within two and a half months of vesting, so there is often no payout flexibility at all once the terms are set. The swing shown earlier comes from how the vesting itself is structured. A benefit that vests in tranches over several years spreads the income over those years; a benefit that vests all at once does not. That structure is decided in the plan document, which is negotiated individually for each executive, so the moment with the most leverage is before you sign, not after. Controlling the size of the spike beats every after-the-fact attempt to offset it.

Bunch charitable giving into the vesting year through a donor-advised fund. This is usually the cleanest way to put a real dent in the ordinary-income spike. If you give to charity anyway, the vesting year is the year to do it in volume. By front-loading several years of intended giving into a donor-advised fund, you take the deduction in the year your marginal rate is highest. Cash gifts are generally deductible up to 60 percent of adjusted gross income and gifts of appreciated securities up to 30 percent, and donating appreciated stock instead of cash also sidesteps the capital-gains tax on the appreciation. You decide where the money goes to charity later; the deduction lands now, against the spike.

Max every pre-tax account available that year. Each dollar into a pre-tax account is a dollar of ordinary income removed in the year you most want it gone. In a vesting year, fully fund the 403(b), a governmental 457(b) if you have one (its limit is separate and stacks on top of the 403(b)), and a health savings account if you are eligible. The dollar amounts are modest next to a large vest, but the offset is pure, and the cost is nothing.

Plan state residency around vesting and payout. A large income event is taxed by the state you are a resident of when it lands. This does not reduce the federal bill, but for an executive considering a relocation, it can entirely erase the state layer on the spike. If a move is on the horizon, the timing of vesting relative to that move can meaningfully change the total tax.

Coordinate the rest of the return around the spike. A vesting year is the wrong year to stack additional discretionary income. Push Roth conversions and other elective income into the lower-income years around the vest, not on top of it. This does not lower the spike itself, but it keeps you from compounding it.

Use the re-deferral window where it exists, carefully. Where a plan is governed by Section 409A in addition to 457(f), pushing a payout further out generally requires electing at least 12 months before the scheduled date and deferring an additional five years or more. This is a real lever, but it is governed by strict rules, the timing is unforgiving, a late or mishandled election can trigger immediate tax plus a 20% penalty, and whether it is available at all depends on how your specific plan is written. Miss the window and you are locked in.

An advanced option: For executives who are qualified purchasers, meaning roughly five million dollars or more in investable assets, certain trader-fund partnership structures can generate ordinary losses that offset ordinary income, including a vesting spike. These are genuine tools, not capital-loss strategies, but they carry full hedge-fund fees, real investment risk, illiquidity, and tax treatment that sits in a gray area some tax academics expect could face future scrutiny. Most executives with a typical 457(f) are below the eligibility threshold, and even for those who qualify, the tax benefit should never be the only reason to hold the investment. It is worth understanding and worth a careful conversation, but it is a narrow fit rather than a general answer.

Why coordination wins

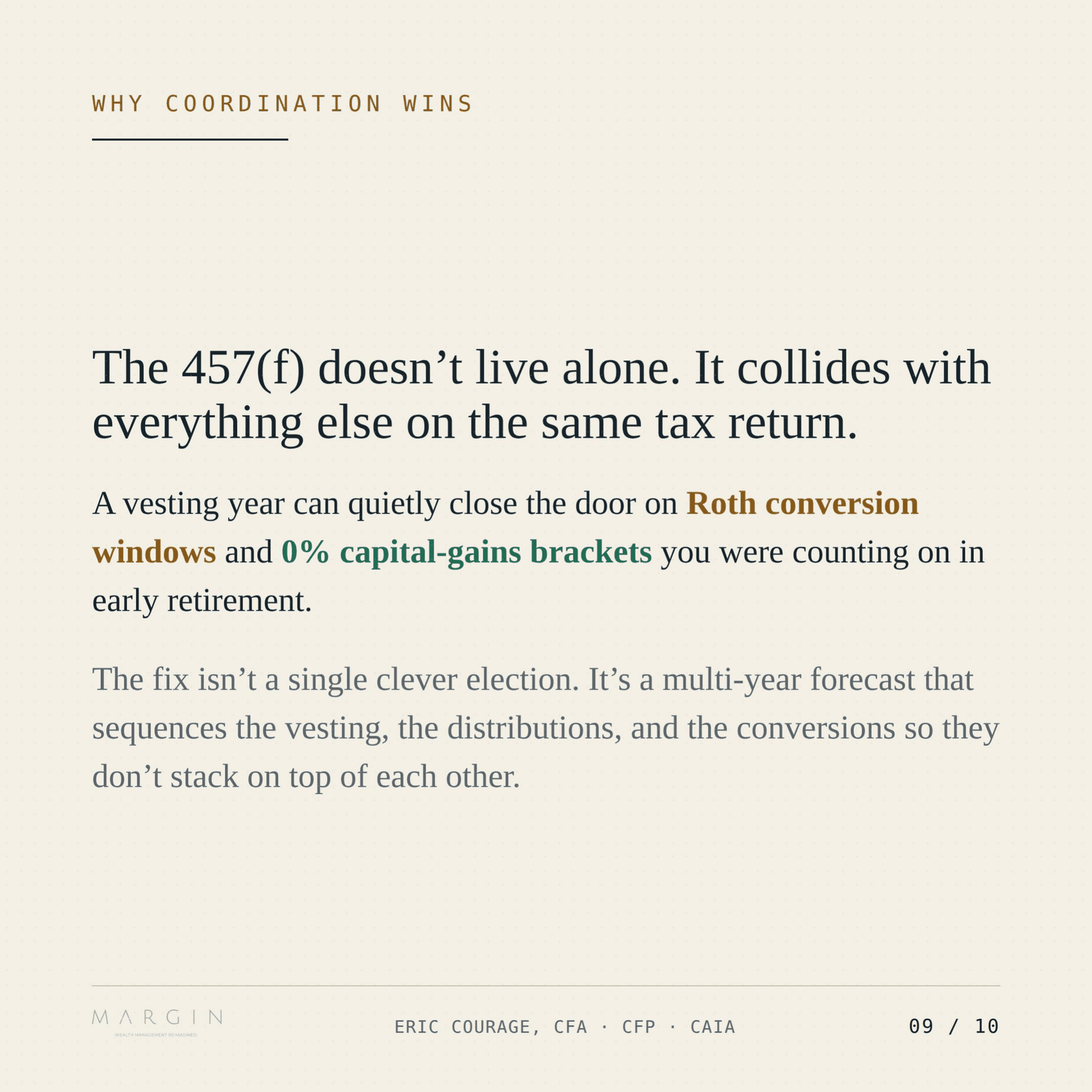

The 457(f) does not live alone. It collides with everything else on the same tax return. A vesting year can quietly close the door on Roth conversion windows and the 0% capital-gains bracket target you were counting on in early retirement.

The fix is not a single clever election. It is a multi-year forecast that sequences the vesting, the distributions, and the conversions so they do not stack on top of each other. That sequencing is most of the value, and it is the part that is almost impossible to do well in the vesting year itself, once the options have narrowed.

The bottom line

A 457(f) can be a powerful piece of an executive compensation package. The benefit is real, the deferral is valuable, and for the right person, it is a meaningful part of building wealth. But it is taxed on its own schedule, at vesting, and that schedule rarely matches when the cash shows up. The leaders who do well with these plans treat the vesting year as a known, plannable event years before it arrives, not a surprise to react to.

MARGIN is a fee-only RIA in Denver, Colorado, serving senior executives nationwide. This article is for general educational purposes and is not tax, legal, or investment advice. Your specific situation may differ, and you should consult a qualified professional before acting.